You've got your startup off the ground and created what seems like the perfect budget. But as the months pass, you notice a gap between budgeted and actual expenses.

Sounds familiar? Well, you're not alone. Welcome to the world of budget vs actual.

It’s something all business owners struggle with, especially new ones. The good news is that you can get much better in planning over time, with lessons learned from your previous budget variance analysis.

The question is – how? In this article, we'll explain everything you need to know about budget vs actual variance analysis with plenty of tips to keep you on track.

To see how the budget vs. actual variance works, we need to define them first.

A budget is a plan that outlines how much money a company expects to make (revenue) and spend (expenditures) over a specific period, like a year. It sets targets for various financial aspects like income, costs, cash flow and other factors that measure a company’s success.

Actuals, on the other hand, are the real numbers that show what a company has actually earned and spent over the same period. They reflect the true financial performance of the company.

Imagine a small business that plans to earn $100,000 in a year and spend $80,000 on salaries and supplies. This plan is the budget. At the end of the year, the business checks its accounts and finds out it earned $90,000 and spent $85,000. These are the actuals.

In this case, the result is a $15,000 smaller profit, which is disappointing, but somewhat acceptable. In other cases, unwise financial planning could even lead to coming out at a loss at the end of the year.

In simple terms, a budget is like a map of where the company wants to go, while actuals show where the company ended up.

Comparing the two is necessary to see whether you've achieved your financial goals, and if not – why and what you should do differently next time.

For example, when finance leaders track these actual numbers for the first time, they might discover surprise costs or expenses not planned for in the budget.

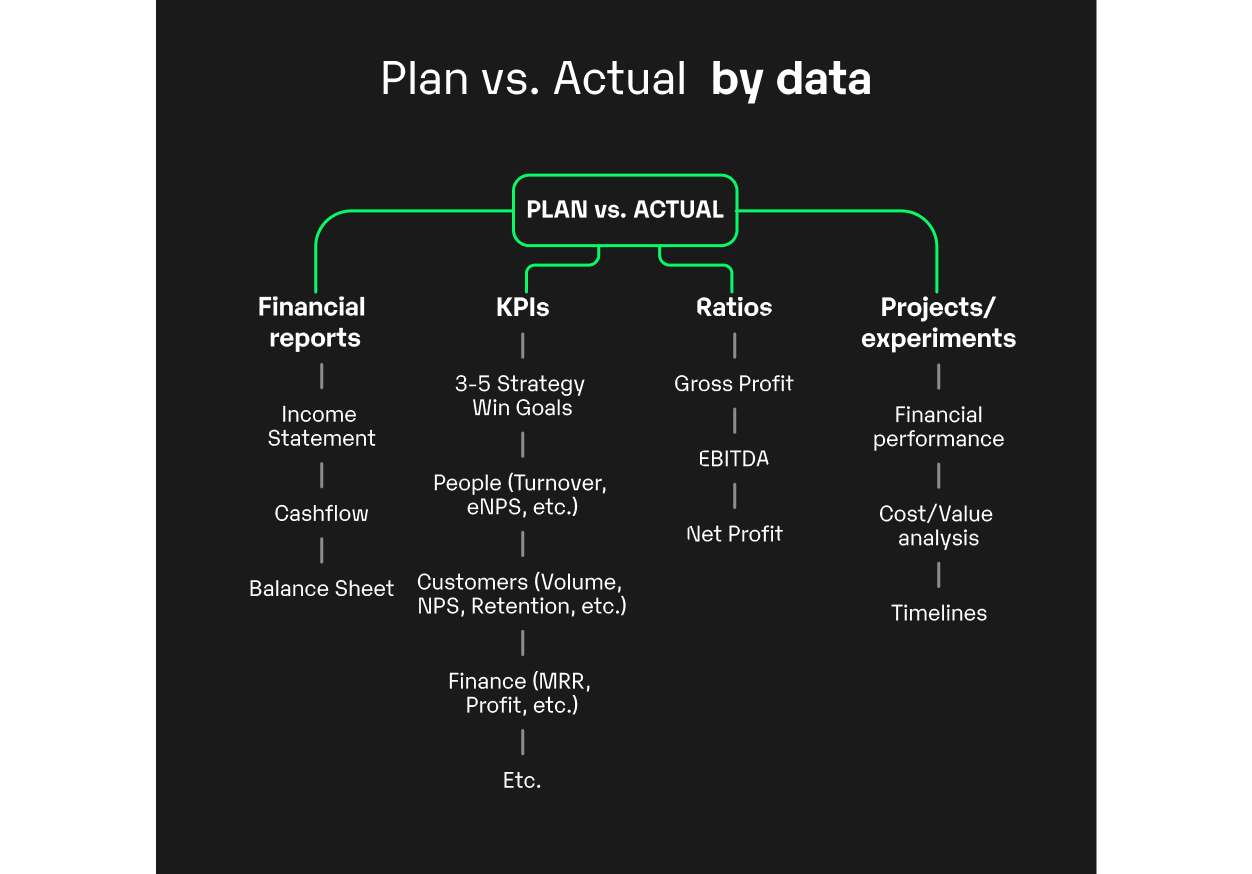

Budget vs. actual can cover the following data:

Contrary to some advice you can find online, it's not enough to do budget vs actuals once or twice a year. We suggest doing it more regularly, to the point it becomes a habit.

By keeping an eye on actual results, you can tell whether your company is on track to meet its goals. If you notice something is off track, you can adjust the budget to get back on course.

There are four periods you can use to get insights into budget vs. actual and those are:

This is the typical formula for calculating budget vs. actual:

Actual sales or expenditures / Budgeted or planned sales or expenditures (expressed in %)

Certain factors significantly affect unfavorable variance in small business financial planning and budget planning in general, such as:

You should especially watch out for recurring and increasing losses. Here are four tips to avoid these:

Finally, make it a habit to go over the budget results in team meetings regularly. Discuss where the company is doing well and where it’s not meeting its financial goals. Make sure that everyone understands the reasons behind any budget variances.

Remember that budget planning isn’t always about aiming for the biggest possible monthly profit. The goal isn’t always to save money. For example, let’s say you planned to spend $10,000 on marketing over a particular time period, and you ended up spending only $1,000.

This isn’t necessarily a good thing as it means you haven’t adhered to your marketing plan and probably won’t attract as many new clients as you planned, affecting your long-term goals and revenue.

Hold executives and department heads accountable for their spending decisions and how they impact the company’s finances.

Many companies create excellent financial plans, but these often get forgotten and remain just unfulfilled dreams in spreadsheets. For a plan to be effective, track your progress regularly and analyze the actual results as you progress.

Here's our 8-step planning process:

Every successful financial plan starts with an idea, but not every great idea becomes a winning strategy. Here's how to ensure success and make your ideas come to life:

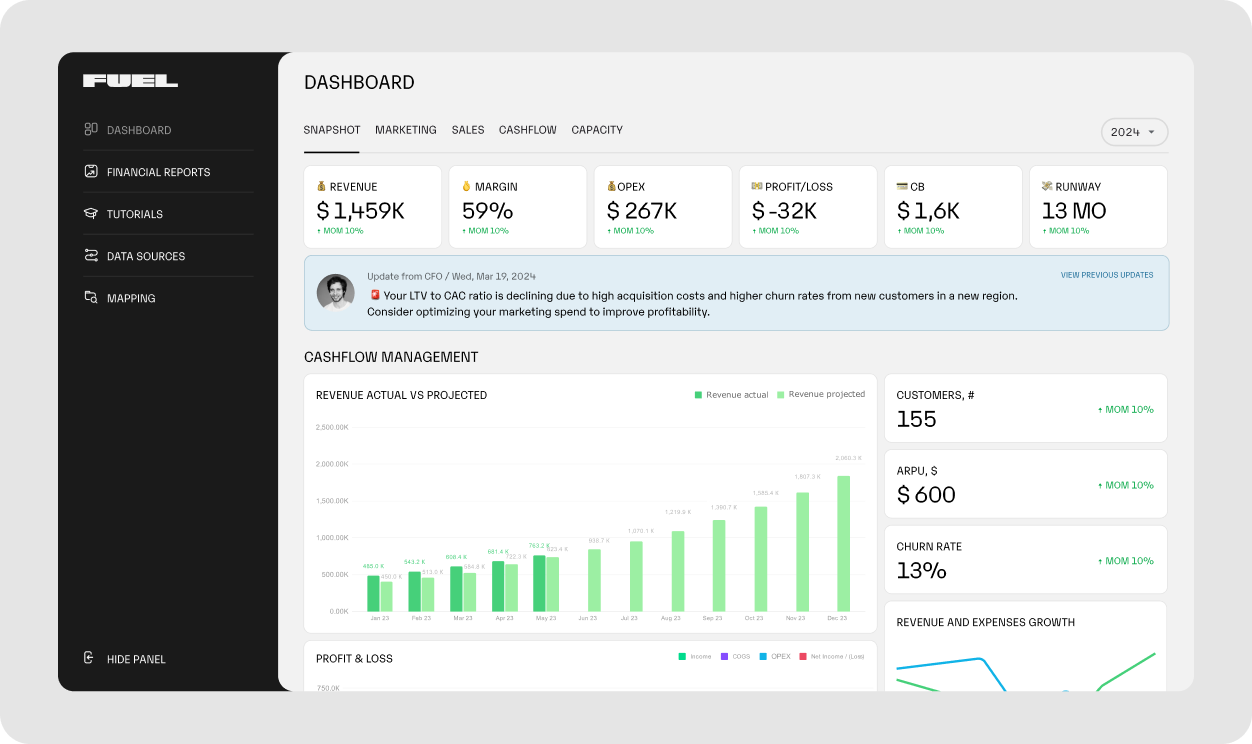

The best way to do budget vs actuals analysis is to pull your data from your financial software. If you're using Fuelfinance, you can see all your metrics in one dashboard. Plus, we also recommend KPIs tailored to your startup financial model.

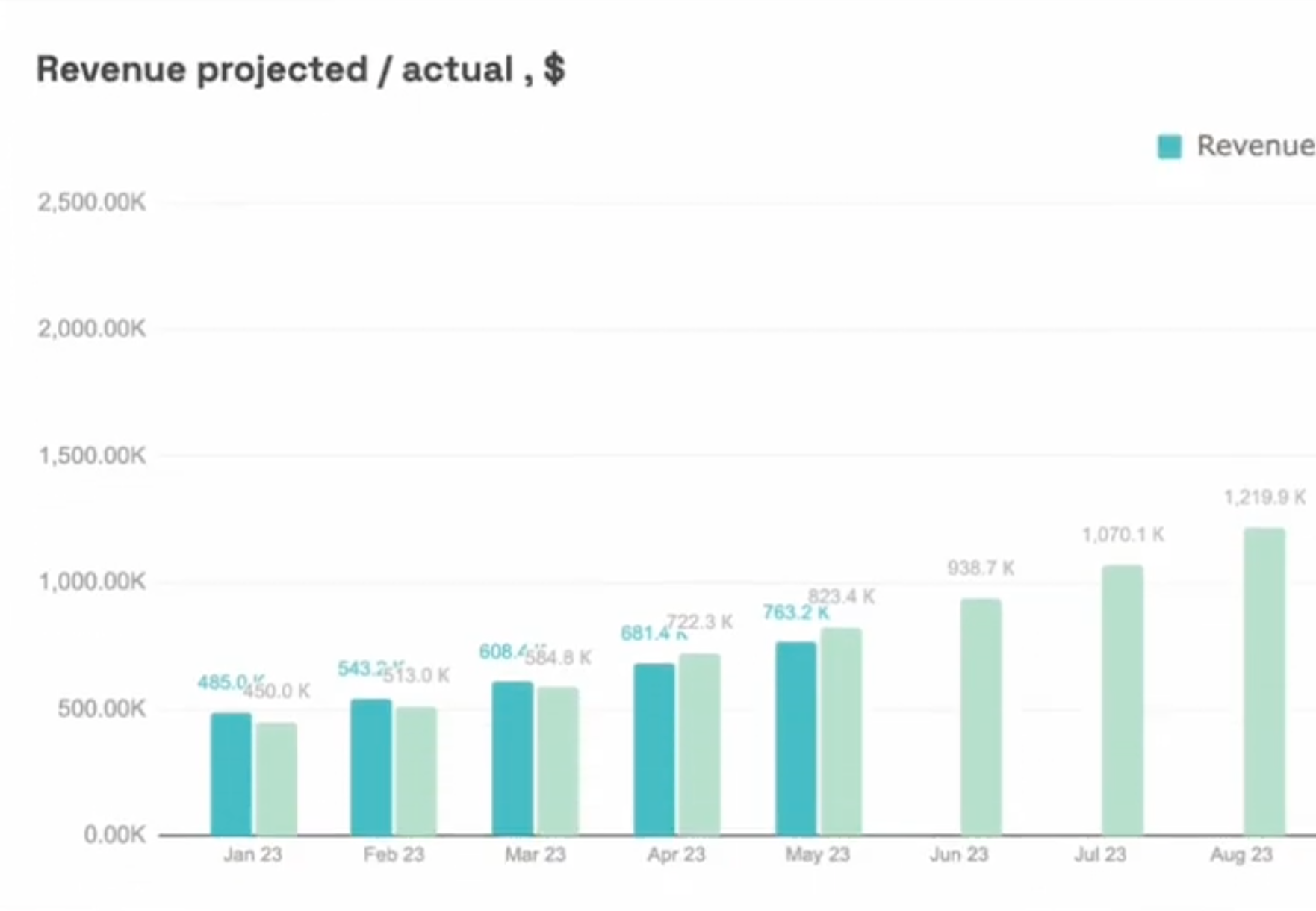

The best thing about Fuelfinance is that you don't have to calculate anything. Our dashboard updates in real time and you can clearly see the difference between projected and actual revenue, as in the picture below.

Scroll further in the dashboard to see a detailed breakdown of each metric.

Here, you can see the difference between your projected income and actual income over a particular period (in this case, it's a positive, or favorable variance, meaning that your revenue is higher than you projected).

Then, you can see the outflow, or how your actual expenses compare to what you've planned, whether you've spent more or less, and exactly how much.

If you notice negative variance (earning less than you projected or spending more than you planned), ask yourself two questions:

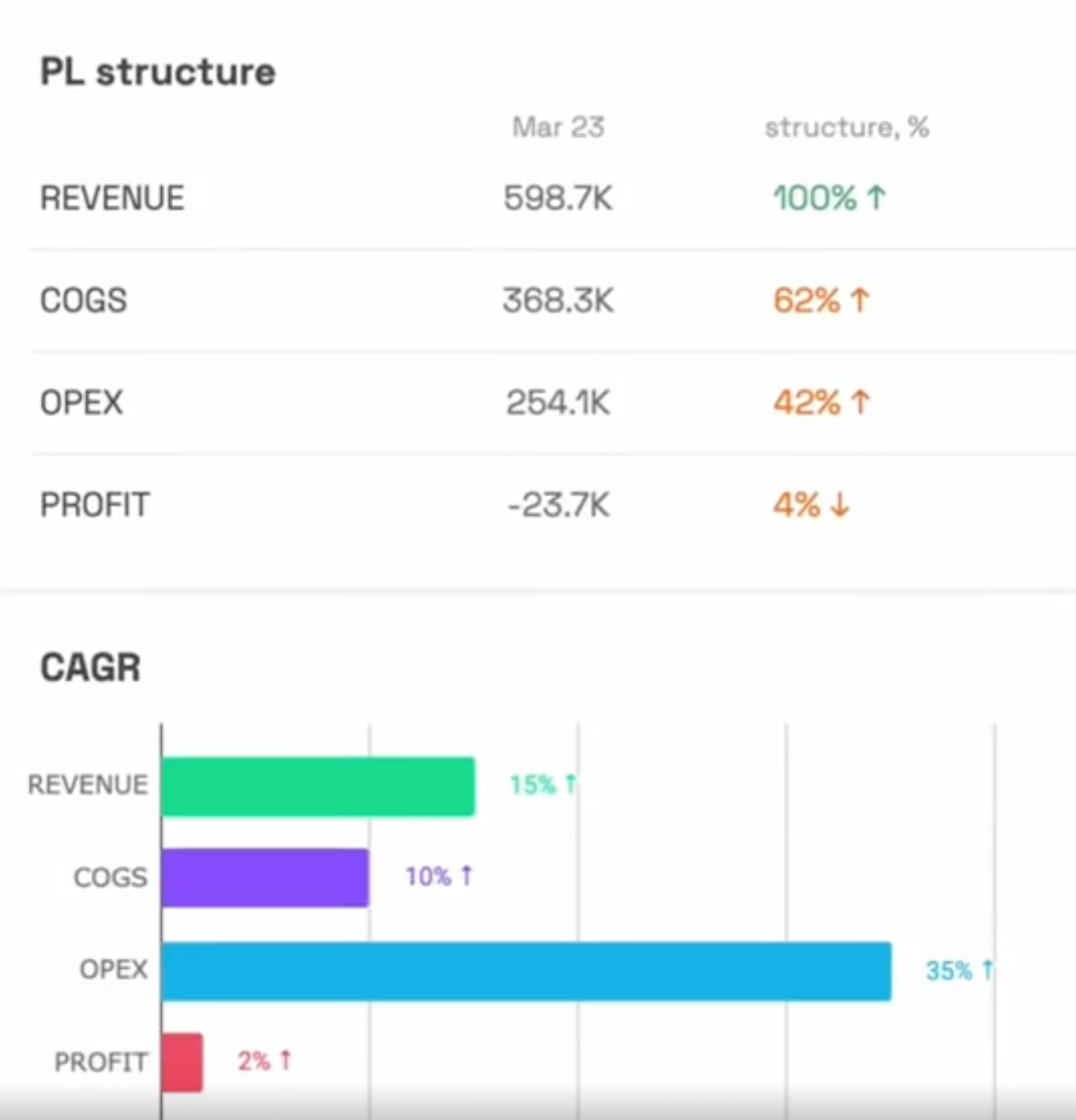

When you finish analyzing the budget, you can move on to other metrics like revenue, COGS and profit in the same dashboard.

Would you like a financial expert to guide you through each step of plan vs actual analysis? If you’re nodding your head in agreement, download our cheat sheet where we’ve summed up everything you need to know.

FORM FOR GETTING THE CHEAT SHEET

Get our Plan vs Actual

cheat sheet.

Plan smarter 🤑

hbspt.forms.create({ region: 'na1', portalId: '23433501', formId: 'c0666823-92ec-4f9a-bcbd-3b6121b513a0' });

At Fuelfinance, we believe you don’t need to be a financial whiz to understand your finances and do a budget vs actual analysis. With the right financial planning software tools and a little help, every startup founder or small business owner can easily handle their company’s finances (not just variance reports).

That's why we've created small business financial management software tailored for startups. It comes with unlimited support from our finance team, which acts as your outsourced CFO.

Our tool helps you create accurate projections and financial models that will reduce your expense variances and allow you to take control of your finances.

Here are its key features:

If you're an early-stage startup without funding, we’ve got something for you. Check out Bootstrap, a free tool that helps you manage business finances and create compelling reports for investors.

Click here to discover what investors really want from early-stage startup finances.

With Bootstrap, you can:

Starting a business comes with its own challenges, and at Fuelfinance, we understand that. That’s why we’ve developed easy-to-use financial software tailored for small companies and startup founders. Our solution simplifies financial management, even if you’re not a finance expert.

Fuelfinance keeps your books in order and calculates crucial metrics such as budget vs actuals. These figures show your business’s profitability and performance. Our software also assists with revenue recognition and financial statements.

You’ll also have ongoing support from our team of experts, who are ready to answer any financial questions.

Ready to see how Fuelfinance can streamline your financial management?

Book a demo today, and let us show you how simple your financial journey can be.

A budget is a plan for how much money a company hopes to make and spend in a year. Actuals are the real numbers showing what the company earned and spent during that time.

In a budget, “actual” means the real money that has been spent or earned. It shows you what happened compared to what you initially expected.

Budgeted costs represent the estimated amount of money planned for something. The actual cost is the real amount spent.

First, find the difference between the resources you planned to allocate and what you actually spent. If you've used more money than planned, this number will be positive. Then, divide that number by the planned amount and multiply by 100 to get the percentage you went over budget.